Quarterly Market Recap : April 2024

Capital Markets Recap

• The strength in the US economy continues. After real GDP growth of 3.1 % in 2023, the narrative among economists has changed to a soft landing with real GDP projected to grow 2.4% according to the St. Louis FED.

• The strength in the US economy continues. After real GDP growth of 3.1 % in 2023, the narrative among economists has changed to a soft landing with real GDP projected to grow 2.4% according to the St. Louis FED.

• Employment continues to be strong with unemployment at 3.8%, and new claims have been moderate. This could change somewhat as new minimum wage laws in California have led to many fast food restaurants to close.

• The decline in inflation has stalled and remains elevated partly due to a strong economy and high Federal spending making it harder for the Federal reserve to bring inflation down to its goal of 2.0%.

• The S&P 500 had a strong 1Q24, increasing 10.2% led by Communications and Energy with energy benefiting from the US oil price rising 20% from the end of 4Q23 to the end of 1Q24.

• The 10-year Treasury bond yield increased by 32 bps during the quarter to reach 4.20% leading to a decline in bond prices. The Aggregate US Bond Index declined 1.3% in 1Q24.

• We favored intermediate term bonds, but recommended investors to stay away from long-maturity bonds since continued large US deficits could force the yields on long-bonds higher leading to price declines.

• We recommend bond ladders of Intermediate bonds with attractive yields and the potential for price appreciation in the next2- 3 years .

• Short term interest rates remain at attractive levels, but have reinvestment risks once the FED lowers interest rates which we expect in 2024 and in 2025.

• Studies show that market timing typically produces inferior returns. We encourage diversification and a focus on working towards financial planning goals.

Economic Data Points As Of

Unemployment 3.8% 5-Apr-24

10 Yr Treasury Rates 4.54% 10-Apr-24

30 Yr Mortgage Rates 6.82% 4-Apr-24

CPI YOY 3.5% 10-Apr-24

US GDP Growth Q4 2023 3.4% 28-Mar-24

Model Portfolio Positioning

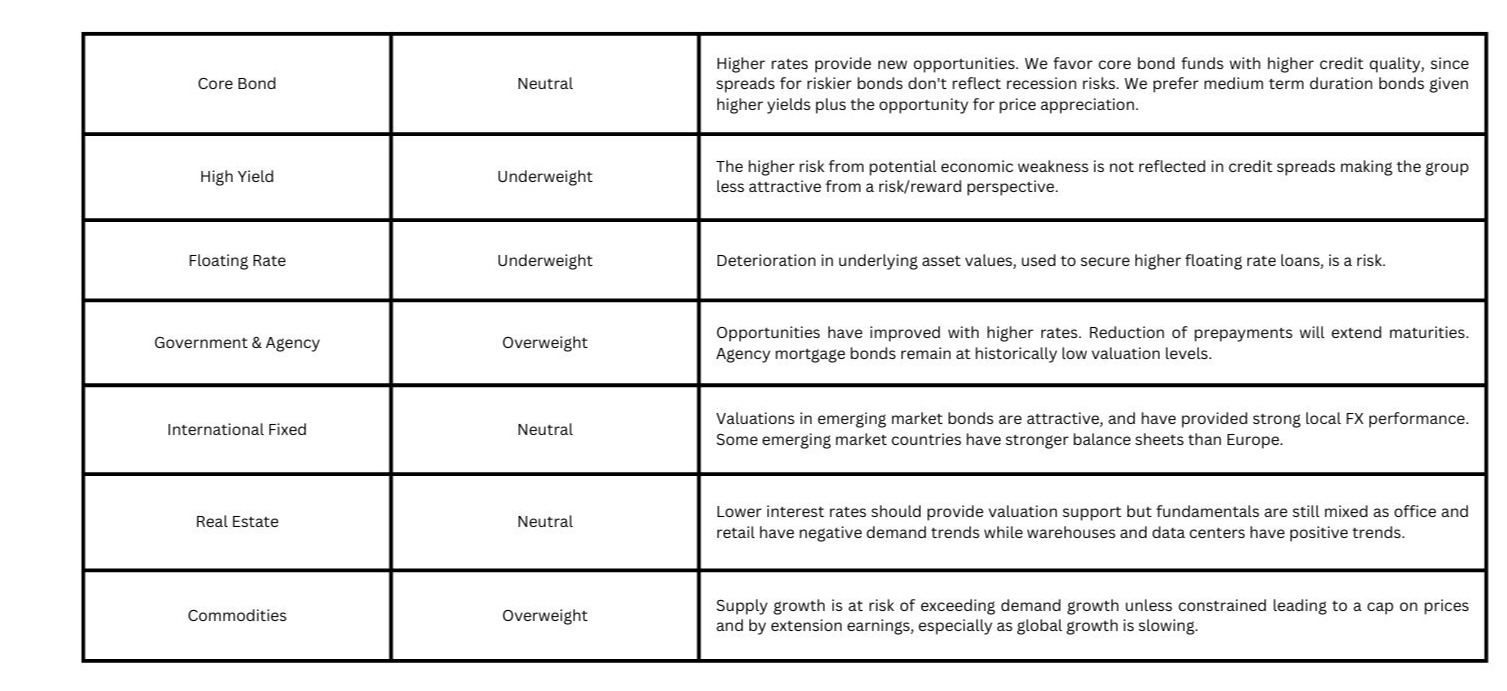

Fixed Income & Alternatives

Equities

Looking Ahead

- Geopolitical unrest and the risks to global growth:

- Global unrest has escalated in the last two years following Russia's attack on Ukraine. The recent Israeli killing of two senior Iranian generals in Damascus has led to an Iranian call for retaliation. This could increase tensions further in the Middle East and risks a miscalculation that expands the conflict beyond current Gaza and Yemen/Red Sea/.

- We need to recognize that Cold War 2.0 has started with Russia, China, and Iran on one side and the West and allies on the other side. The delineations are less clear than in the past, but increased tension and separation will have negative consequences for trade, globalization and economic growth as resources are allocated away from consumers to defense.

- Economic growth, unemployment, and FED action:

- The US economy continues to grow keeping unemployment relatively low which is positive for consumer spending. The FED has signaled the next move is a reduction in interest rates, but the pace of reduction could be much slower than prior thought due to persistent high inflation.

- The corporate sector remains strong as 2023 earnings came in better than expected at the beginning of the year and this has led to higher projections for 2024 earnings. As companies continue to hire more workers, it should propel the economy higher.

- US Government budget deficits:

- The US continues to run large budget deficits with the first six months of fiscal 2024 coming in at minus $1.1 Trillion despite a 7% YoY increase in tax revenues. With both Presidential candidates being populists, we don't expect any change in spending, only where the spending will go post the election.

- US Government Debt:

- US Federal debt-to-GDP has risen to 122% versus 58% in 2000. The Congressional Budget Office (CBO) projects US Federal debt-to-GDP will continue to rise in the next decade even in the most positive scenario.

- Continued large budget deficits will make this worse and eventually force harsher changes when the music stops.

- Interest payments on the Federal debt held by the public rose 43% YoY in the first six months of fiscal 2024 to ~$440 billion, exceeding defense spending of $412 billion for the same period.

- As the interest on the Federal debt will consume a higher, and higher percentage of the government's budget, it will crowd out other spending, making it harder to make changes the longer we wait.

- Increasing debt from low debt levels is not a problem. It becomes an issue when debt levels are so high adding more debt and refinancing existing debt becomes problematic.

- FED action and Capital Markets:

- Higher interest rates increase the cost of capital for all companies. This means fewer projects get approved, ceteris paribus, and by extension lower future growth.

- The risk of bankruptcy for highly indebted companies increases as interest costs rise faster than revenues.

- Ultimately, higher interest rates are negative for both the stock and bond markets. The higher rates lead to a higher discount rate for future growth, that also is lower, leading to lower equity valuations and to lower bond prices for existing bonds so yields can be competitive with coupons on newly issued bonds.

- Emerging market growth and China's real estate bubble:

- China has become less dominant in the EM due to the overhang of bad debt from large real estate developers that will keep economic growth subdued given the country's dependence on the real estate sector for growth.

- Companies are moving production away from China with India being a big beneficiary as the country's economic growth has surpassed China.

- Higher demand for key raw materials used in the energy transition will benefit select EM economies such as Brazil and Indonesia that have these resources.

- Economic growth, corporate earnings, and financial markets:

- Putting it all together, we expect the US economy to continue to do well in 2024, aided by US corporate earnings growing DD. We favor intermediate IG corporate bonds due to a combination of strong balance sheets and attractive yields. We recommend long-term investors to stay invested as patient investors were rewarded well in 2023, but recognize continued large US budget deficits and higher Federal debt will increase risks over time.

Disclosures

These are the opinions of Ascend Wealth Planning, LLC and not necessarily those of Cambridge, are for informational purposes only, and should not be construed or acted upon as individualized investment advice. Investing in securities involves risk of loss. Further, depending on the different types of investments there may be varying degrees of risk Clients and prospective clients should be prepared to bear investment loss including loss of original principal. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors. Diversification and asset allocation strategies do not assure profit or protect against loss. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is not a guarantee of future results. Registered Representatives offering securities through Cambridge Investment Research, Inc., a broker-dealer, member FINRA/SIPC and Investment Advisor Representatives offering advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Advisor. Cambridge and Ascend Wealth Planning, LLC are not affiliated.